Eddie Brissett, The Brissett Group LLC and First Place Realty Group LLC, Pena Realty Corp.Phone: (617) 816-1426

Email: [email protected]

Email: [email protected]

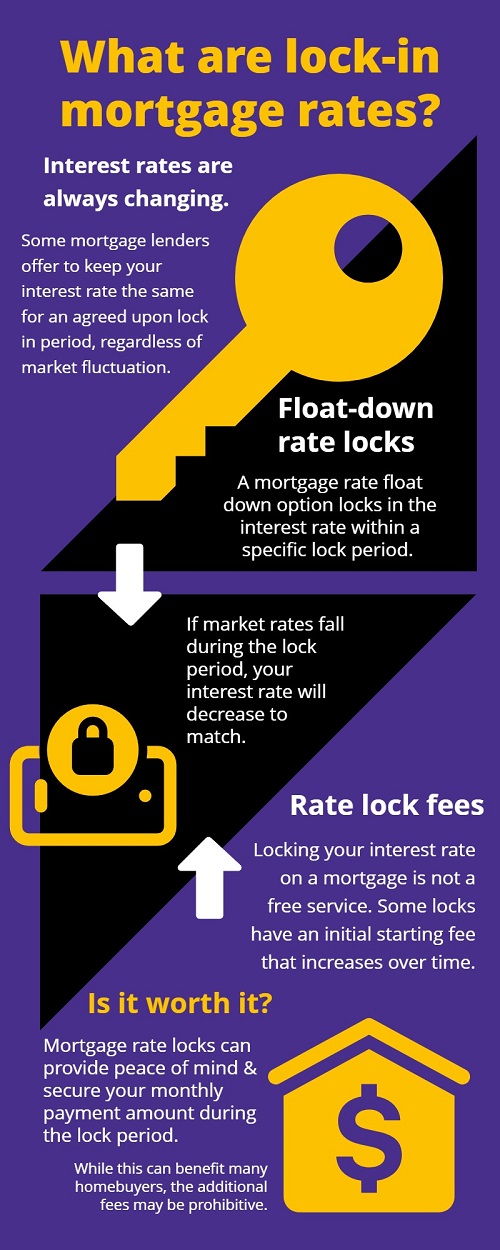

With mortgage rates constantly fluctuating, many lenders offer the ability to lock in a specific mortgage rate. These provisions keep your interest rate the same for an agreed upon lock in period, regardless of whether national rates fall or rise.

However, while a rate lock period can have its advantages, it's not the right answer for everyone. Here is some more important info about mortgage interest rates and locks for homebuyers to be aware of:

If you lock in interest rates on a mortgage loan, you can secure them from the time of approval until five days before closing. However, the lock only lasts until the end of your current loan, meaning your interest rates will no longer be locked if you refinance.

Therefore, timing your mortgage rate lock is crucial - you might even be able to get a lower rate on your second mortgage as well.

A rate lock has far fewer disadvantages than risk. An interest rate lock does not help to get the cheapest mortgages, but rather safeguards your buying power. The rate lock prevents a mortgage's interest rate from increasing and potentially pricing you out of your own home due to high monthly mortgage payments.

Various banks can lock the rates with what are called "float down" provisions. In these cases, the rate is lowered in a specific period after the loan approval. Whenever the price increases, your payment will match what you're quoted for.

While this can benefit many homebuyers, there is a risk that rates will never change in your favor. This would result in paying higher interest rates for the whole term.

Having a rate-lock may reduce your mortgage costs, but the process isn't free of charge. Generally, rate locks include a fee starting an initial amount, which increases over time. In some cases, mortgage lenders will charge a fee for extended locks. Make sure to go over the options carefully to avoid any unpleasant surprises down the road.

Should you accept a lock-in rate from your mortgage lender? Keep these factors in mind to make the best decision for your financial future.

Eddie Brissett is a native of Newburyport, Massachusetts where he attended Newburyport High School. He graduated from Fitchburg State College (FSC) with both a B.S. in Business Administration and an MBA in the late 1990s. He also played basketball at FSC.

In 2004, his real estate dream began when he purchased his first property- a condo. Working primarily in financial services for nearly 15 years, he transitioned into real estate full-time in 2013. He was the Condo Board Chairman (2005-2018) of the Rich Street Condo Association. He credits his parents and mainly his mom as among the biggest influences in his life. As a licensed real estate agent in several states, he serves buyers, sellers, renters, and landlords throughout the commonwealth of Massachusetts, Rhode Island and Florida.

"From an early age, I learned the value of hard work and standing by your word from my parents. These traits along with teamwork were reinforced from some tough sports coaches that I played for."

He enjoys spending his free time with family, friends, hiking, watching Boston sports teams, and is an accomplished billiards player.